By Kersten Heineke, Timo Möller, Asutosh Padhi, and Andreas Tschiesner

We often hear people ask, “Who will be the winner in the transformation the mobility sector is facing?” As autonomous driving, shared mobility, connectivity, and electrification disrupt the industry, there is uncertainty about who will come out on top: traditional players or new entrants, the hardware or the software guys, Western or Asian companies, product or service companies? In our perspective, however, success in the emerging personal-mobility landscape will depend less on what individual players are doing today and more on the choices they make regarding tomorrow’s strategic direction.

In our first article on the acceleration of the automotive revolution, we offered an integrated perspective on two key questions: What is the speed of change, and what do the new value pools look like? In this one, we present our perspective on the logical third question: What is required to successfully navigate the emerging personal-mobility landscape in an uncertain future?

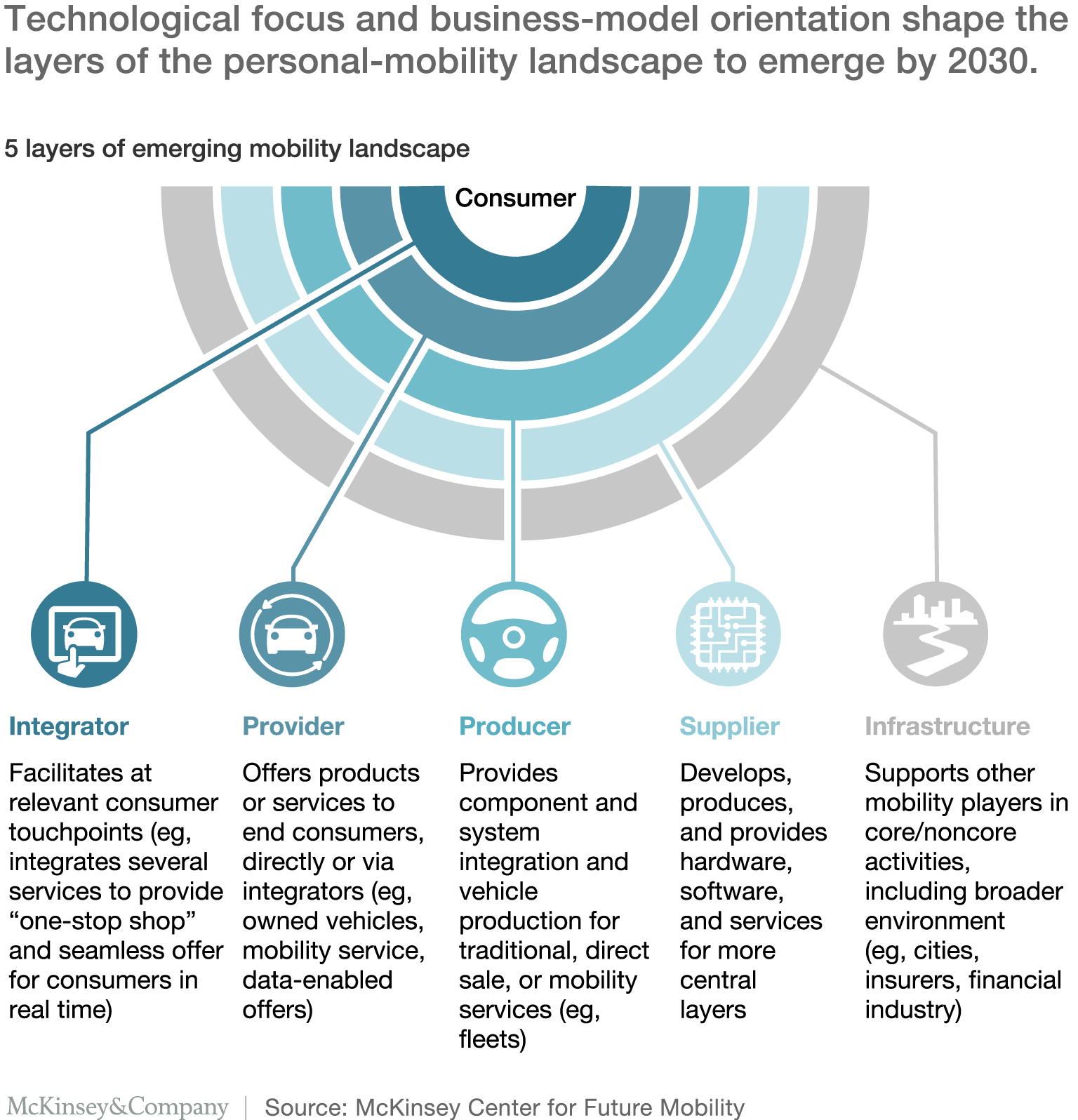

The previous piece introduced the concept of a new personal-mobility landscape in which players move beyond rigid roles and, instead, may employ more than one business model, engage multiple technologies, and be active across mobility layers as their capacity to deliver value to their customers allows (Exhibit 1).

In this article, we take a deeper look at this landscape to identify themes related to how industry players might actually accomplish this.

Successfully growing or transitioning into the new mobility industry will require more than simply defining or reorienting a fixed strategy. Strong navigators will learn how to choose based on probabilities. At the same time, they will remain agile and not fixate on a single road forward. As such, mobility players should take four actions, which we will discuss in more detail: define their strategic posture and select differentiating capabilities to build, choose their individual strategic setup, pursue optimal partnerships, and actively manage the transition from traditional to disruptive models.

1. Prioritizing capabilities to realize a healthy strategic posture

The future of the mobility industry is characterized by uncertainty. As such, there will likely be several ways forward due to the impact of regulations, technological disruptions, and divergence of consumer needs, for example—each unfolding at a different pace. Players thus need to think about which developments they consider more probable than others and how well they are positioned to follow those paths toward successful outcomes.

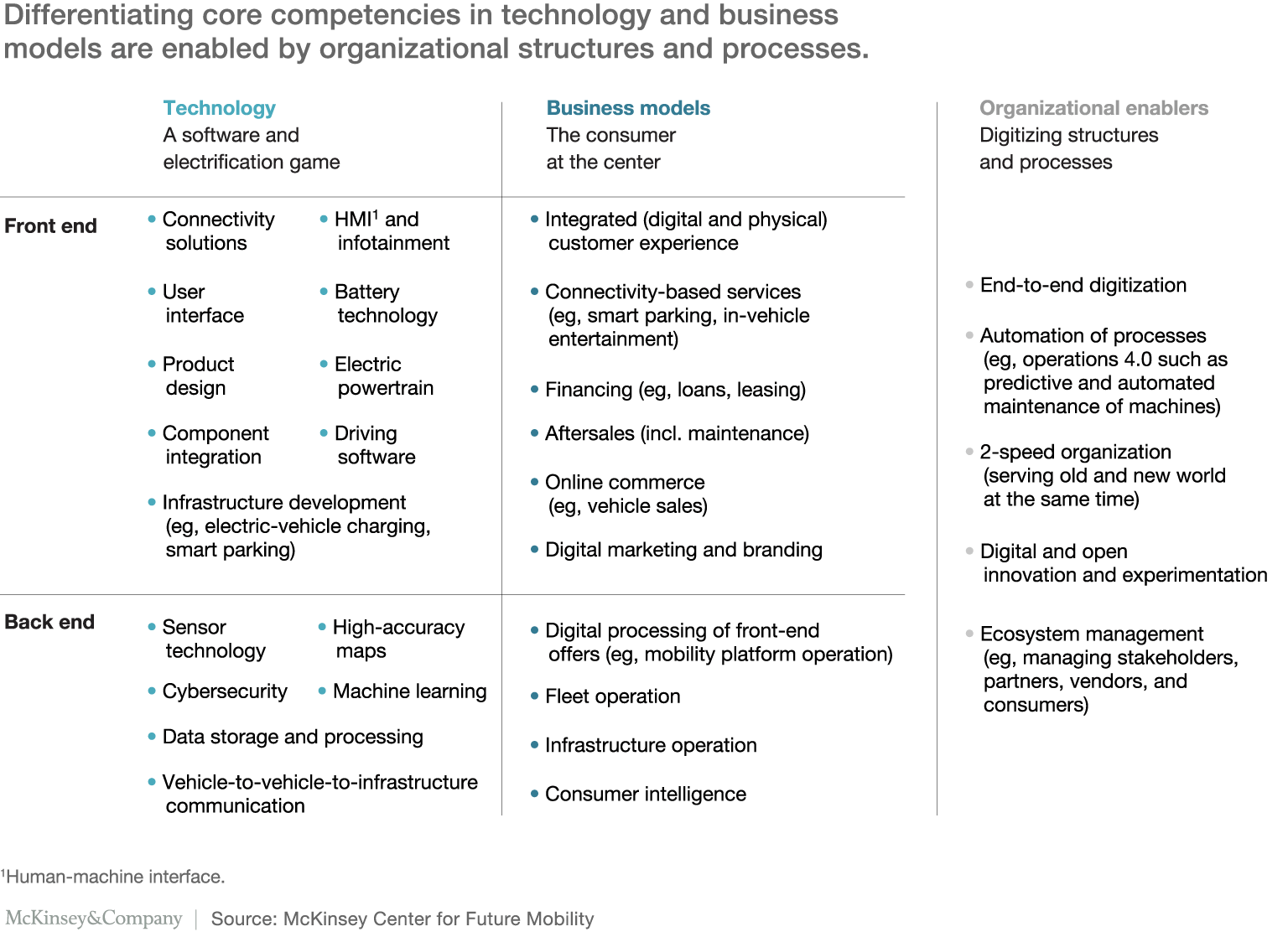

In doing so, identifying relevant technology and business-model competencies that will allow for differentiation is an important step and should be taken early on in order to define a suitable strategic posture. On the technology side, mastering software capabilities or creating advanced skills in electrification may become key areas for successful differentiation. Similarly, in considering where to focus concerning business-model competencies, it could be critical to choose competencies using a customer-centric perspective.

Moreover, trends in the space will also require players to develop a robust organization that enables capabilities around digitization, automation, and innovation, for instance, to the point that they are able to compete along their newly chosen core competencies.

Taking a closer look, we find 25 competencies in the areas of technology and business models, which can be clustered into front-end and back-end competencies, as well as five organizational enablers (Exhibit 2). Companies must master them all to successfully differentiate and serve consumers across all four disruptive trends (autonomous driving, shared mobility, connectivity, and electrification). And most differ from what traditional players have become used to refining for decades, such as a skill set around optimizing the development of internal combustion engines (ICEs).

Beyond building such a multitude of competencies, achieving at least a defensible position in-house for each of the four technology-driven trends would require an established automotive manufacturer to commit to investments totaling more than $70 billion. This conservative estimate is based on the probable number of attractive products a player would need to offer to compete in a given space and the necessary enablers required in bringing those products to market.

Our analysis found that the bulk of the cost of disruption will fall to players supporting traditional automotive business models that need to deploy significant capital to develop technologies while bringing new products and vehicle models to market. As such, building new electric-vehicle (xEV) platforms, converting existing ICE platforms, and rolling out semi- to fully autonomous technology to a sufficient number of models (as a share of the fleet of a typical mass-market OEM) may cost at least $55 billion over the next 15 years.

There is a lower cost to entry for new mobility business models, such as building a shared-mobility service in a specific region or developing a connectivity platform for in-vehicle services and advertising. To compete in just one of these two verticals, a company should be prepared to spend roughly $5 billion to $10 billion in the same time frame.

This is a high level of investment. And, as our estimates represent the likely overall cost of entry, further funds may be necessary to achieve a leading position in any one of the trends, as competitors will probably make similar moves simultaneously.

No single player is apt to “do it all,” so incumbents and new entrants alike will have to define their strategic posture clearly—that is, where they want to shape, follow, wait, or even exit the mobility industry. Defining this stance includes prioritizing core competencies and the areas of the mobility landscape they may occupy, identifying partnerships that will widen their reach, and mapping the path to their envisioned end state as a successful mobility player.

2. Choosing a mobility strategy based on a clear profile of qualifications

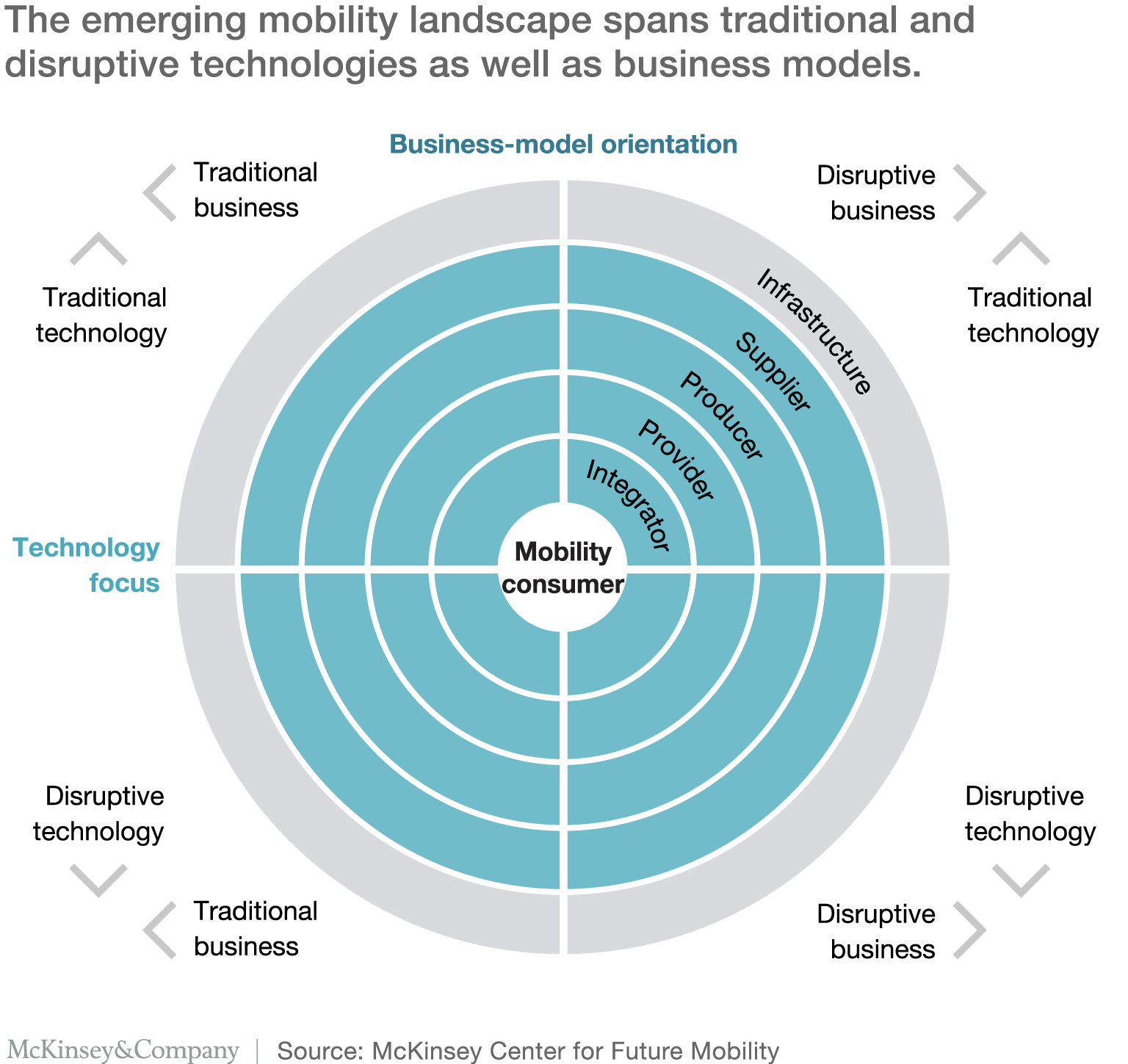

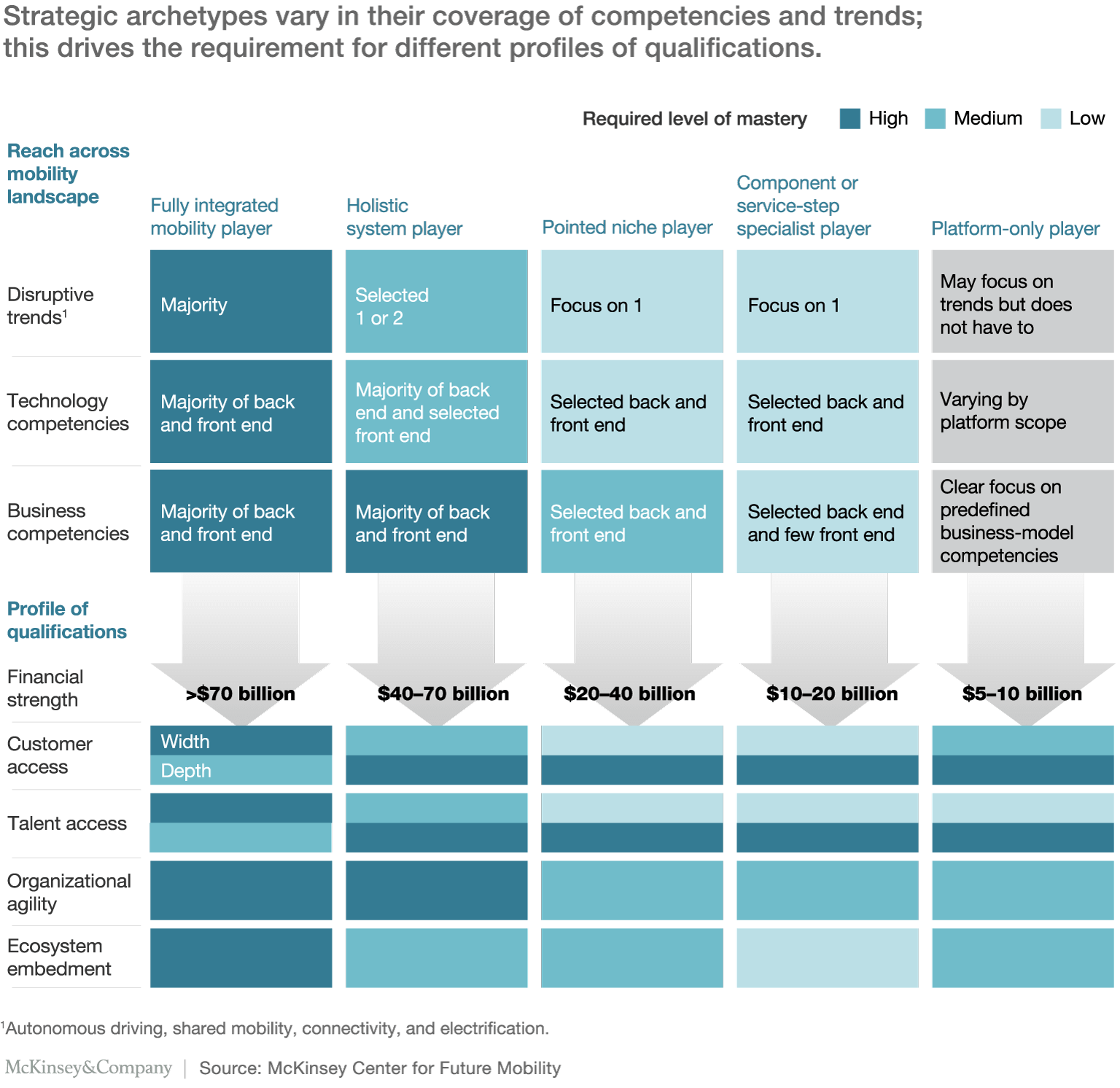

To build up the new mobility landscape, all segments in all five layers will have to be fully served (Exhibit 3). Individual players will have an ever-growing number of ways to compile their offers and define their mobility strategy in line with their aspirations.

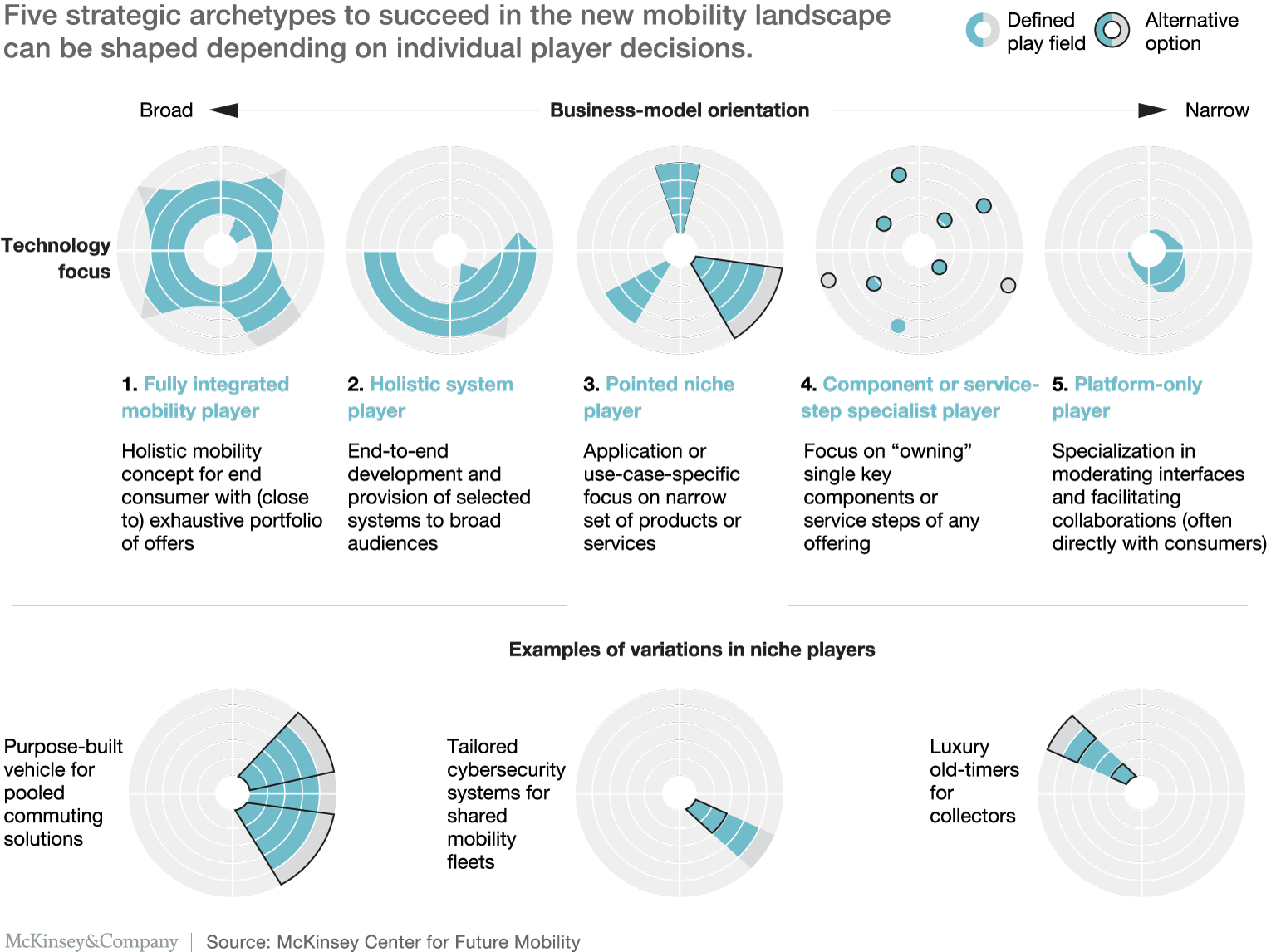

Looking at the potential breadth of any actor’s portfolio, we see five strategic archetypes evolving. Each archetype looks quite different in its coverage of the personal-mobility landscape. Even within each of the archetypes, different subtypes can evolve, depending on where players decide to focus and how they fine-tune their approach (Exhibit 4).

To succeed within each archetype, players must carefully select and master a minimal set of technology and business-model competencies, as we outlined in Exhibit 2. For example, a “pointed niche” player may decide to bet on one trend—say, autonomous-driving technology—and therefore, depending on the planned focus, will need to cover all software-based front-end and back-end technology competencies. This player might need to build advanced machine-learning capabilities, double down on driving software, and create the relevant set of business-model competencies such as the effective processing of front-end offers.

To offer a complete and differentiated portfolio within a selected archetype, a company—such as the autonomous-driving niche player—will need to have a minimum profile of qualifications. Five characteristics should be considered in selecting the most suitable strategic archetype:

- financial strength, that is, the minimum available funds and the ability to invest effectively in accordance with the selected strategy over the course of five to ten years

- customer access, that is, the level to which one has wide access to the relevant base (for example, serving a broad range of different customers across segments, needs and wants, demographics, and geographies) or deep access to build relevant knowledge and serve effectively (for instance, understanding a specific customer type down to daily routines, individual wants, and needs)

- talent access, that is, the opportunity to widely (across a broad range of disciplines) or deeply (through specific knowledge in a selected field) recruit and retain relevant talent—such as software engineers or designers—given the employer’s attractiveness

- organizational agility, that is, the ability to quickly adapt significant parts of the organization to a rapidly changing company focus (by adopting structures, processes, or employee skills to new market requirements, for instance)

- ecosystem embeddedness, that is, the extent to which one is or can be networked with relevant partners and vendors in a targeted field or the broader mobility landscape

Accordingly, each strategic archetype demands excellence across a unique combination of various competencies as well as specific qualifications (Exhibit 5). Players looking to be successful in a given archetype will need to build their capabilities with respect to their current individual portfolio of skills and assets.

Companies that understand their profile and the archetype requirements can quickly grasp when a specific strategy could be met or exceeded, or in which circumstances underdelivering might become a risk. Identifying individual nuances can clarify appropriate archetypes and then help players fine-tune their strategy once a choice has been made.

Imagine, for example, a company that aspires to become the standard provider for holistic autonomous-driving technology kits. The company has the necessary expertise in software, is well networked to also cover required hardware components, and has a strong employer and consumer brand. While this sounds promising for a holistic systems-player strategy, the company is also financially well-equipped and could therefore consider becoming an even broader player in the industry, potentially moving into the domain of a fully integrated mobility player instead of focusing on a single system. It is then up to the company to evaluate its strategic posture and preferred way of moving forward in the new mobility landscape.

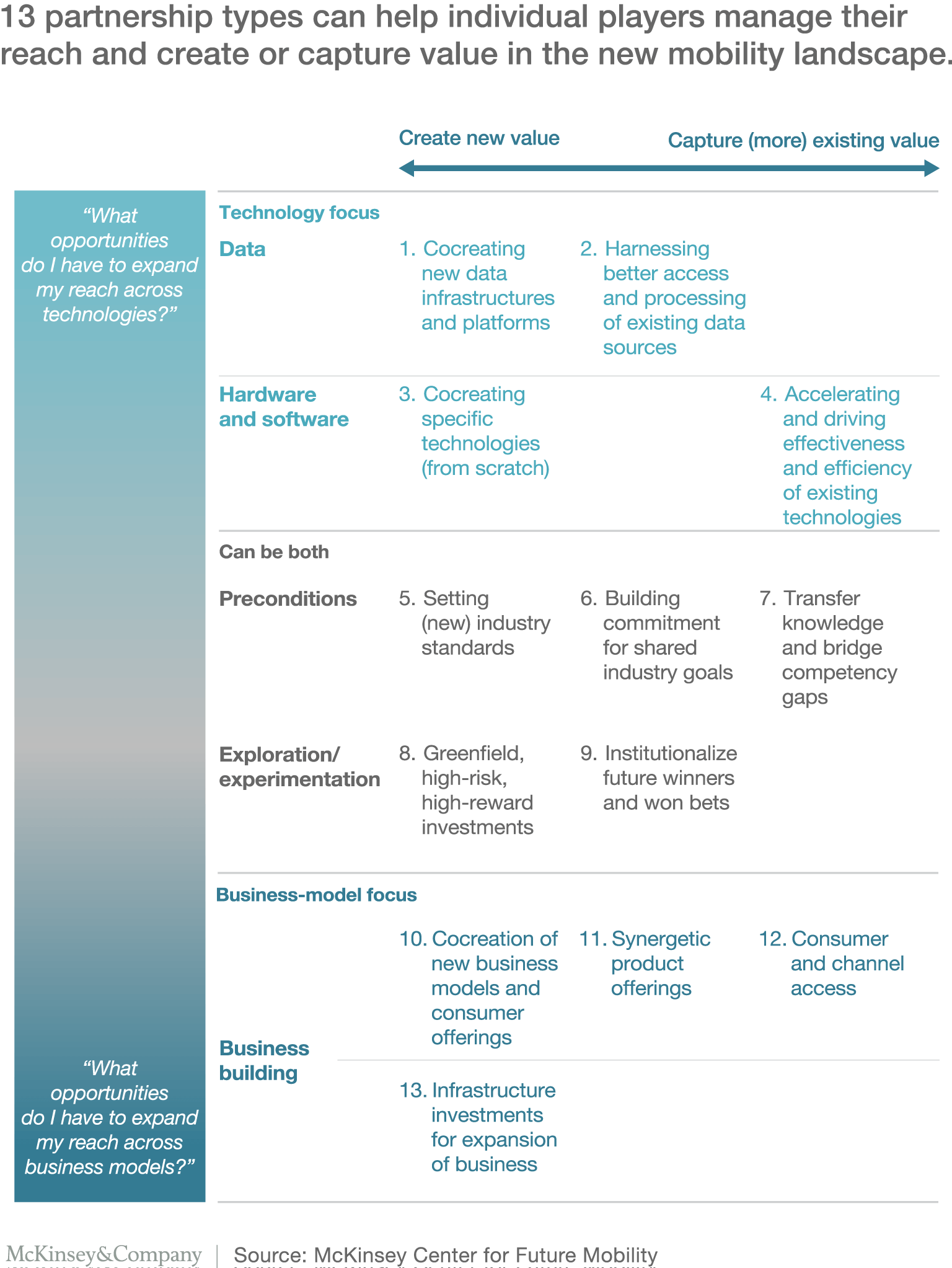

3. Forming the right partnerships for managing reach across technologies and business models

Besides gaining clarity on where and how they want to position themselves, players need to think about how they can extend their reach in the mobility landscape and build relevant partnerships for future success. We have identified 13 types of partnerships, each of which offers a specific approach to help manage a player’s reach across technologies and business models, and to create and capture additional value (Exhibit 6).

Partnerships, by nature, are unlikely to be a fixed construct. They may vary by area of the mobility landscape, as well as by the core competencies they are best suited to cover. For example, dedicated partnerships for setting new standards in the industry may, generally speaking, be well suited to cover technology and business-model topics but should ideally be oriented toward disruptive offers, such as how to think about and handle the deployment of robo-taxis, once available. By contrast, partnerships on synergetic product offers primarily focus on expanding business based on existing technologies and thus can be optimally used for a gradual transition into more disruptive business models.

At the same time, as new partnerships grow more mature, they will probably include more elements of capturing existing value, even if they originally set out with the goal of creating entirely new value pools. Consider a newly established platform for sharing data on autonomous-vehicle behavior: while at the beginning such a partnership may be focused on opening up new opportunities for its contributors, it may shift toward securing the created—and potentially other existing—value pools.

Selecting where to partner, the most suitable type of partnership, and the right structure will not be straightforward as the industry becomes more complex and diverse. Players will presumably face an increasing number of potential partners across all layers of the mobility landscape and from a large set of industries that are all looking to serve the mobility end consumer.

Not surprisingly, we already observe many new offers stemming from rather unconventional partnerships in the mobility space. Take, for instance, competitors collaborating on high-definition maps or new players from different industries such as retail and fashion building on opportunities from fully connected vehicles and car data-enabled services (for more, see sidebar “Example partnership models around Lyft”).

As advances in mobility continue, we expect more and rather diverse partnerships to evolve. For example, multiple industry players have already started discussing the need for autonomous-vehicle remote-control centers, which would serve to help navigate highly autonomous cars in unexpected or emergency situations. Such centers could play a crucial role in getting autonomous technology off the ground and achieving an initial, critical level of adoption, for example, through providing consumers and safety authorities with a sense of security, knowing there is a defined fallback mechanism to start with. A variety of stakeholders, including regulators, fleet operators, and AV-system providers, may be interested in controlling these centers in the future.

On a less concrete level, we could include making electric vehicles serve as mobile power banks for businesses and private households, leveraging autonomous vehicles for more attractive storage or even real-estate deals, or basing entire interior-design businesses on equipping purpose-built vehicles of all kinds. However such partnerships are structured, the future is likely to bring interesting collaborations to benefit the industry and end consumers.

4. Actively transitioning from the traditional automotive world to the new mobility landscape

Beyond looking at how to choose the right strategy and partnerships, we also need to acknowledge the automotive revolution as a fundamental transformation of the industry. In our perspective, players should approach it as such—and the rules of transformational change still apply (see sidebar “Key considerations for a successful transformation”).

This may sound like any another transformation, but for the automotive revolution, it will be particularly crucial to draw attention to the business-case element of the upcoming transition. Financial decisions will have to be made in light of the need to serve two worlds: the traditional automotive business, which will still make up a sizable portion of the industry by 2030, and the disruptive, technology-driven trends, which will grow to take over the mobility industry. Defining the right balance across when, where, and how to invest in one field or divest from another will be of the utmost importance.

The impact can be immense, and players in the new mobility ecosystem have very different starting positions based on their current roles and competencies. To quantify the potential evolution of profitability and investment, we ran a war-game simulation that modeled the potential decisions of various players hundreds of times and assessed the effect of competitive dynamics on profitability (Exhibit 7). Through this analysis, we identified three core components of decision making that seem to help determine success:

- Investment focus. This entails weighing the trade-offs and taking a considered approach on whether to be balanced across exposure to disruptive trends or to focus more on narrow competencies.

- Investment timing. The second component involves managing long lead times for technology development and market entry while staggering high-cost investments and deciding whether to front-run industry developments or take a fast-follower approach.

- Agile organizations. Major events, such as regulatory decisions or the entrance of one or two large players into a market, can disrupt a company’s long-term investment strategy while reducing market share and creating downward pressure on margins. Agile organizations must first anticipate and second react to this risk, specifically when significant amounts of capital and corporate focus are committed to one space.

Looking at average performance and top performers across numerous simulations, we also see how fundamental dynamics for different player types inform various strategies:

- New mobility and platform players. New mobility players start from a position of tight profits and constrained cash flow, but with organizations that are potentially quite agile. These players could see massive expansion of their current profits, achieving growth of a hundred times or more. However, they must carefully position themselves to respond aggressively to potential new entrants and changing regulation that could dethrone them.

- New technology and specialist players. Large technology players and specialized companies focused on bringing one or two disruptive technologies to market have the luxury of timing and targeting their go-to-market strategy while working with numerous players to scale technologies and profits across large volumes. For these players, a variety of approaches proved successful; whether manufacturing lithium-ion batteries, developing connectivity platforms, creating in-vehicle-services ecosystems, or even rolling out a shared-mobility fleet, all generated strong returns in competitive environments. With access to large amounts of capital—giving them the ability to decide when to enter, if at all—the key obstacle these players needed to overcome was the ability to identify sufficient OEM partners and the best business models. In our testing, only 30 percent of the simulated companies were able to both enter the automotive market and generate long-term profits.

- Automotive OEMs. Automotive manufacturers faced a more varied path to long-term profits. High levels of fixed capital, long product cycles, and the need to transition to new technologies in the face of an uncertain future mean shareholders of some companies may need to prepare for an intense phase of capital redistribution and pressure on profitability. In our simulations, we still saw various decisions leading to success, but close to half of all simulated strategies resulted in negative or neutral profit growth.

Many large OEMs diversified their bets across a range of powertrain and autonomous systems, keeping core intellectual property and investments in-house and staggering their investments to minimize risk and spread costs. However, in some successful paths, OEMs achieved an even more radical transformation of their businesses, divesting tens of billions of capital from their core ICE business as they shifted large portions of the portfolio to xEVs and advanced autonomous vehicles while rolling out their own mobility platforms.

Smaller OEMs, including emerging-market players and niche-market specialists, were forced to sharpen their focus if they were to succeed. In some instances this meant falling back on producing the core vehicle, while strategically sourcing high-volume disruptive technologies (such as partially autonomous driving systems and hybrid propulsion) to grow their market share at the cost of a substantial profit give-back to the system suppliers. Other OEMs created outsize growth by focusing on one disruptive technology, such as battery electric vehicles or fully autonomous vehicles, building a brand and being first to market at the expense of all other potentially addressable segments.

Our simulations revealed a wide variation in the ability to grow profit across types of players and strategies as the industry goes through a wide-reaching disruption and transformation.

Many of these outcomes themselves were critically sensitive not only to the actions of others and the evolution of overall industry structure but also to exogenous shocks. In the war game, a battery manufacturer could achieve substantial returns by investing in a multibillion-dollar battery-manufacturing facility and supplying to one or two mass-market OEMs. This investment would fail absent the ongoing and increasing regulatory support for xEVs; alternatively, it could generate 30 percent greater returns through improved battery chemistry. Similarly, the success of fully autonomous vehicles represents a paradigm shift for shared-mobility players’ revenues and profits, but technology failure or regulation delaying the rollout could keep that business on a more conservative long-term path and lead to negative returns for players heavily invested in the technology.

The level of uncertainty facing many of these major investments is significant. While our analysis suggests the existence of winning paths, the road to the future is uncharted. But the four key actions we explored here could help players navigate in the emerging mobility landscape. Staying flexible while at the same time learning to operate based on probabilities will continue to increase in importance.

As the pace of technological change in the industry accelerates, we believe the question is no longer whether the disruption will occur. Rather, it’s how quickly and to what extent players will have to reimagine their businesses to serve the mobility consumer of the future. The new landscape will require new technologies, competencies, and partners, while still relying on traditional businesses and products as part of the solution.

The size and potential impact of the automotive revolution requires more than gut feeling to drive the right decisions for a successful mobility strategy. Only a good understanding of the potential outcomes and a data-driven mind-set can enable actors to adjust to the full impact of the disruption on their business. War games, such as the one we conducted, seek not to forecast the future but to simulate a range of possible scenarios and understand how they could affect the profitability of a variety of players. They also allow companies to test their strategies in the face of an uncertain future and enable key decision makers to approach impending changes with an industry-wide perspective.

We hope this article encourages organizations to think about probable futures, decisions, strategic alternatives, the moves of other players, and the importance of a future-oriented vision. The next 15 years will usher in a new mobility landscape, with large shifts in the deployment of capital and the capture of profits. Navigating what’s ahead will require businesses to approach the market with a long-term vision and to clearly communicate with shareholders and partners about the road ahead.

Download The automotive revolution is speeding up: Perspectives on the emerging personal-mobility landscape for a single view of our research on today’s automotive revolution (PDF–1.45MB).