The automotive industry is in the early phases of what is expected to be rapid and fundamental change. The emergence of four trends, in particular, will lead to massive shifts in the business models of traditional automotive companies and open the door for other players who have, until recently, only been indirectly tied to the industry:

- Autonomous driving. As of 2016, only one in 100 vehicles sold were equipped with technology that enabled basic, Level 2 autonomous-driving (AD) features. (Here, we use SAE International’s definitions as laid out in SAE J3016; Level 2 refers to partial automation.) However, 47 percent of consumers surveyed in a 2017 McKinsey survey on mobility say they would feel good if their family members used AD technology.

- Connectivity. Internet-connected infotainment systems are the platforms for delivering a growing set of services to drivers. Most OEMs are already equipping their premium vehicles with fully connected systems, but monetization is weak. However, 40 percent of car owners would switch to another brand for better connectivity—a figure that’s twice as high as it was three years ago.

- Electrification. Less than 5 percent of vehicles sold in 2016 had some type of electric motor. However, in a recent survey, 77 percent of respondents said the electrification of vehicles will make a material difference in reducing environmental impact, and 23 percent would consider an electric car for their next purchase.

- Smart mobility. The range of alternative models for vehicle ownership and usage is diverse and includes car sharing and e-hailing. The fraction of passenger miles traveled using these services today is small, but our customer surveys showed that 67 percent of car owners plan to increase their use of car sharing in the next two years.

Technology is the key to further penetration of all these trends, as well as the developing business models that allow companies to capitalize on them. The industry players—traditional automotive companies and new entrants alike—that identify and secure those technological resources will be best positioned to benefit in the new mobility landscape. Thus, industry players need to think about sourcing underlying technologies rather than acquiring single products or services.

Hunting for technology

New competitors will challenge incumbents by quickly rolling out new business models, as well as by bringing new technologies to the market and capitalizing on them. The big question for all involved will be how to identify which technology capabilities are required for which areas of the new mobility value chain, and how to source them once they’ve been identified.

Sourcing options include, among others, developing new capabilities internally, hiring talent, or acquiring players with certain technological expertise. In many cases, competing successfully will also require cooperation – sometimes even in situations of simultaneous competition. New ecosystems will form along the value chain, as companies with complementary capabilities (for example, software development on one side and deep automotive-embedding capabilities on the other) partner in order to develop and deliver comprehensive offerings.

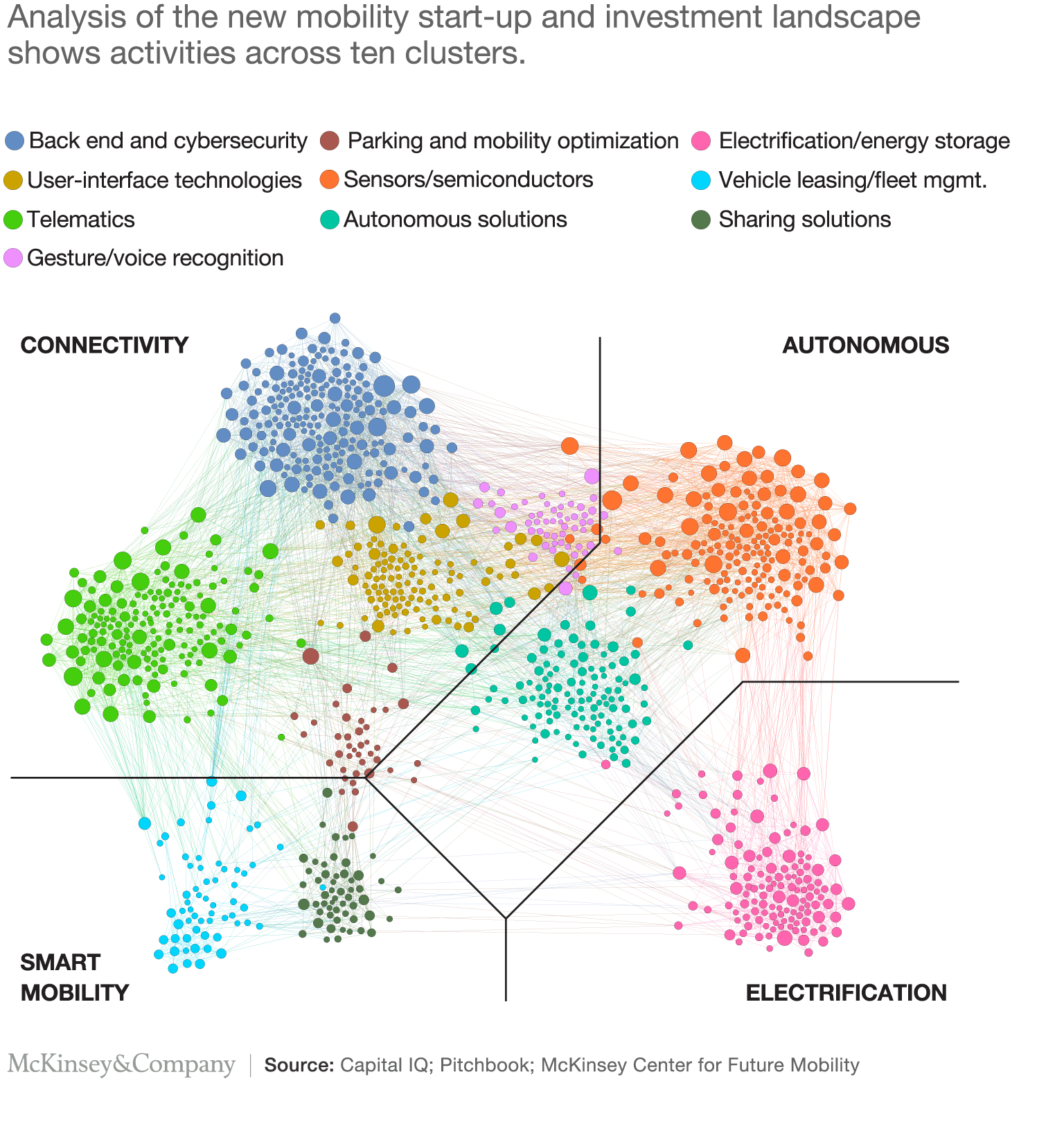

The first steps in building technological capabilities are gaining an understanding of which technologies are most appropriate and differentiating, given a company’s desired role in the new mobility ecosystem, and then finding out where those capabilities exist. Taking an investment view in that journey can be of tremendous value. Investments are usually a good predictor of the future significance of certain technological assets. We’ve developed an approach that analyzes the landscape to dive deeper (see sidebar, “Start-up and Investment Landscape Analysis: A big data tech-finding tool”).

Understanding where the money is going

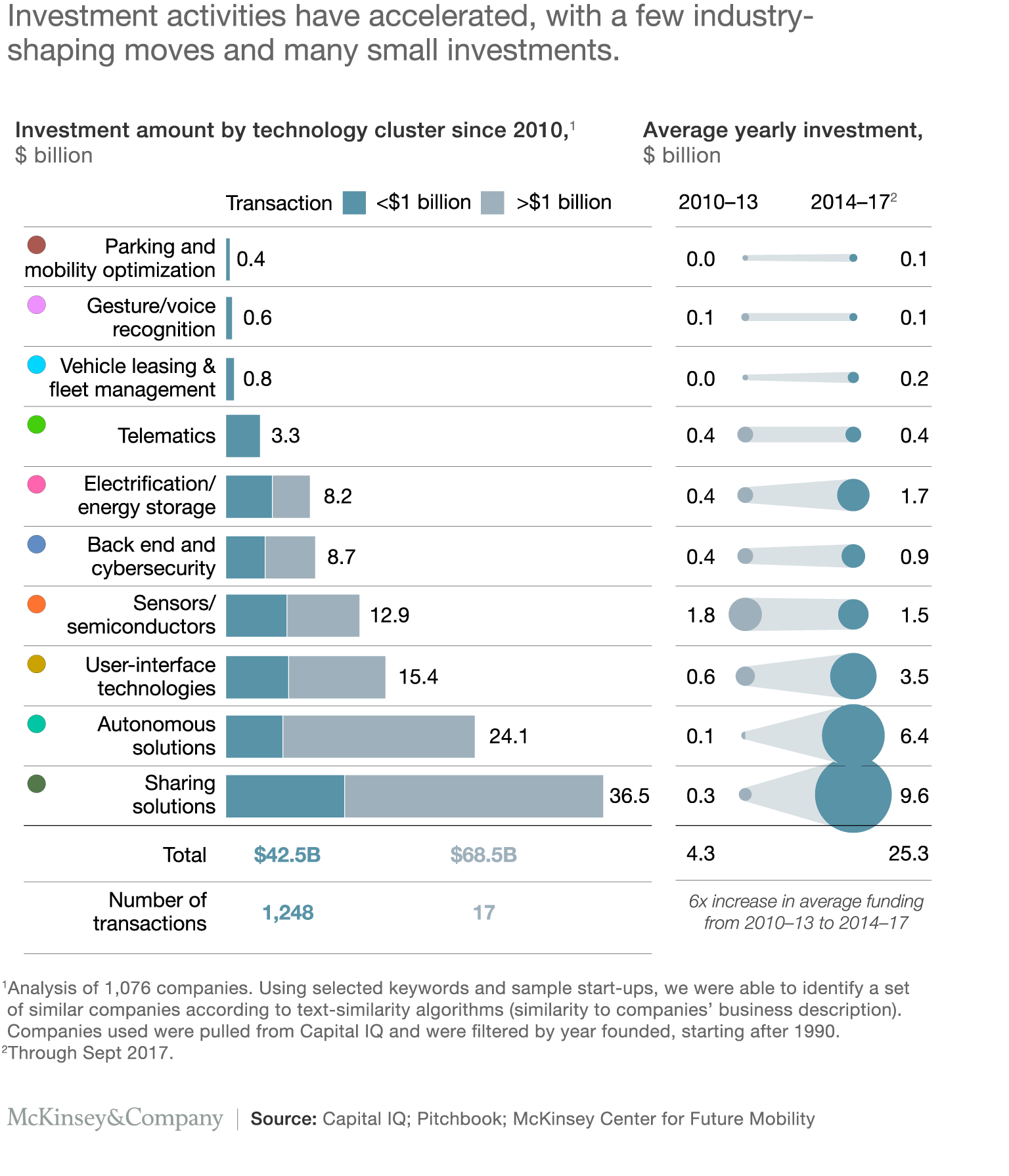

Overall, our Start-up and Investment Landscape Analysis (SILA) tool reveals significant investment activities in new mobility technologies—nearly $111 billion in disclosed transactions since 2010 in more than 1,000 companies across ten technology clusters (Exhibit 1). Surprisingly, less than a third of these relate to shared-mobility companies; the rest focus on the trends of automation and connectivity. Out of the $111 billion, more than 60 percent come from large investments with disclosed transaction values greater than $1 billion, and the rest from small investments. However, one can learn much more from these smaller investments because they are related to smaller companies with special capabilities or technology. The large transactions, on the other hand, tend to be industry-shaping moves made on established companies. Understanding small players and start-ups is crucial to efficient technology sourcing.

To get more granular, we can also break down investments by trend. Of the ten clusters identified, the largest investments were in autonomous solutions and sharing solutions (Exhibit 2). It’s also worth noting that the pace of overall investment is accelerating greatly: between the periods of 2010–13 and 2014–17, the average annual investment across all technologies jumped nearly sixfold, from $4.3 billion per year to $25.3 billion per year. Investments in 2017 to date are as large as the total between 2010 and 2014. While investments in sharing and autonomous solutions account for much of this acceleration, investments in hardware like sensors and semiconductors are rather stable, showing a steady trend of consolidation.

Interestingly, the median annual investment amount per transaction grew by more than a factor of three from 2010 to today—rising from $4.5 million to $15.8 million. Technology is becoming more expensive, and it is getting more difficult to source it, as many are competing for the same players. OEMs with only a few technology-sourcing activities in the past years now face steep costs if they want to access technology via investments in start-ups and midsize companies.

It is also instructive to look at the links between clusters (shown by physical proximity on the node map). The strong interconnectedness of the ten clusters shows the strong links between underlying technologies, showing their wide-ranging applicability—for example, machine learning that is the underlying technology for autonomous-driving software, as well as voice recognition. This is a clear indicator to structure thinking around technology rather than actual services.

In addition to where investments are happening, our analysis also reveals how they are being made. An analysis of all disclosed investments shows that their structure differs significantly by cluster. Investment in autonomous driving is dominated by a few large deals focused on end-to-end solutions (for example, Intel’s acquisition of Mobileye), with a long tail of smaller investments. In the sensor and semiconductor cluster, consolidation characterizes the investment approach, while in user-interface or experience technologies, numerous smaller, specialized players are active.

Geographically, investments are quite concentrated. The majority of investment activity has targeted companies located in the United States (Exhibit 3). Of those, more than half are in the San Francisco Bay Area alone. China and Israel come next. Investments in European companies are small, with German companies accounting for the largest portion, coming in at just over $1 billion. Funding is relatively limited in Germany, though—60 companies there are active in mobility technologies, a number similar to China, which has investments that are over 20 times higher.

This means that non-American mobility players likely will require a footprint in the United States, not just to invest in technology but also to stay attuned to trends, as many are already doing.

Mapping changes in mobility players

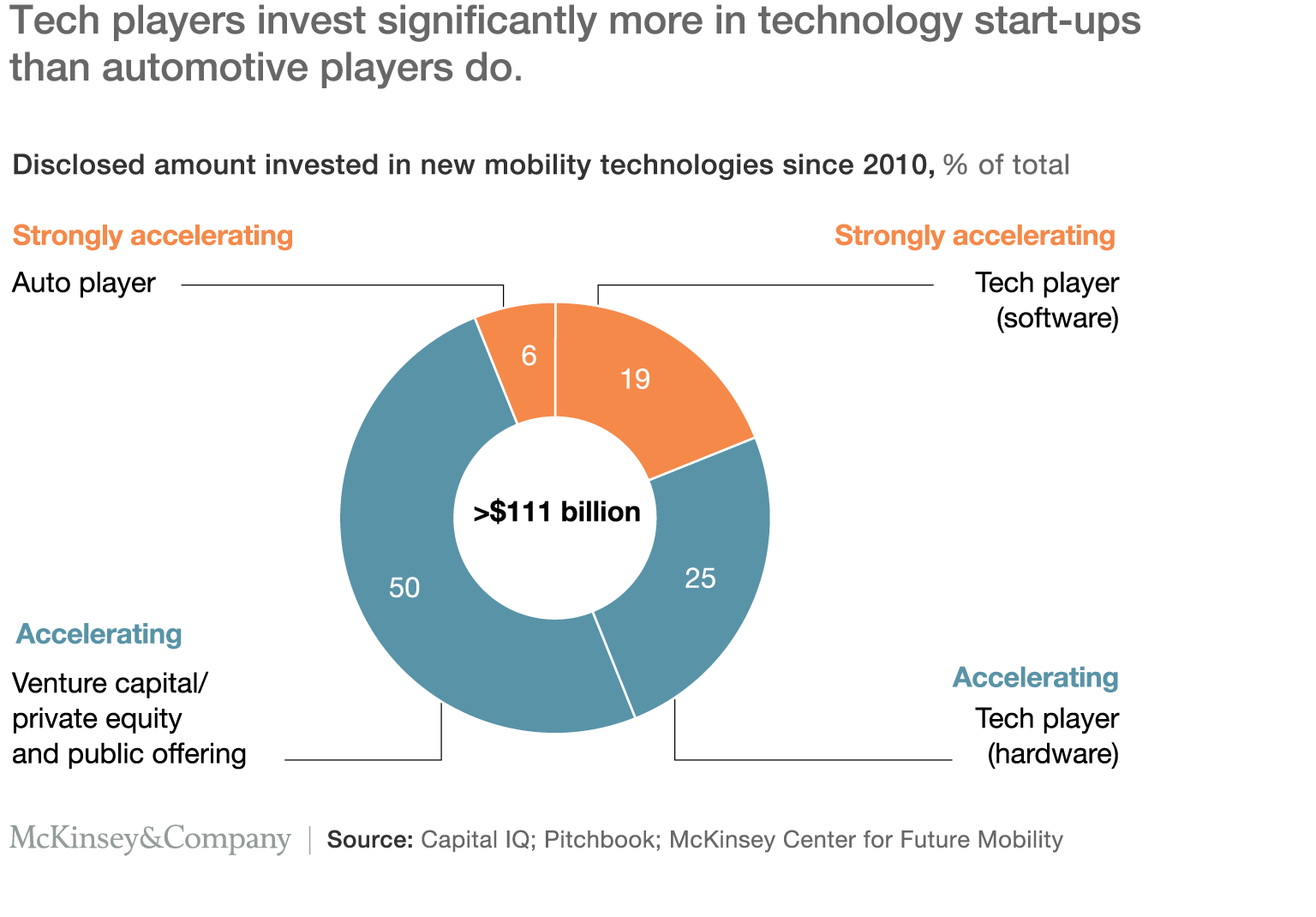

As digital technology becomes a bigger force in automotive and mobility, the face of the “typical” industry player is also changing. SILA affirms this trend in showing that more than 90 percent of investments in the mobility space were made by players not traditionally seen as automotive companies—mainly technology companies, but also venture capitalists and private-equity players (Exhibit 4).

These new entrants are clearly committed to staking their claim in the mobility market, and they are leveraging their digital expertise to make it happen. Of the total investments of $111 billion since 2010, $31 billion was invested in 2016 alone. And of this $31 billion, automotive players invested less than $2 billion (about 6 percent). However, the R&D budgets of auto players in 2016 were $77 billion—more than twice as high as the total investments identified, and nearly 40 times higher than investments by auto OEMs. These players need to take action if they want to stay in the race for technology.

Setting a winning pace in the tech race

Our analysis shows that the race for technology is intense and gaining speed, with major external players entering the space. As it gets more crowded and more diverse, the cost of that technology rises—only investments in hardware are not accelerating. This does not necessarily mean that incumbents need to attempt to outspend new entrants. They will, however, need to position themselves relative to tech companies and define their own technology strategy, including securing access to the technologies they’ve identified as potential differentiators.

To do this successfully, companies must move beyond an anecdotal approach and toward a structured method of technology sourcing. In this respect, traditional automotive players may employ strategies such as purchasing or investing in companies, forming partnerships or alliances, or developing new kinds of tier-one relationships (such as close collaboration partnership houses). The sourcing approach should depend on the dynamics of each technology cluster, as well as the individual company’s strategy. Many small players, for instance, develop innovations in the field of user-interface technologies, making an M&A-like approach possible. On the other hand, large technology players dominate the voice-recognition technology space (for example, BMW plans to integrate Amazon’s Alexa technology), making partnership approaches viable.

The first step, however, will be for automotive companies to identify the use cases and technologies that matter to them and that will be differentiating in the long term. By identifying the relevant technological control points along the value chain—say, driving software, connected services, or human–machine interfaces—they can pinpoint required capabilities. With clarity around these decisions, automotive companies can then determine potential sources of such technologies. This path is applicable to suppliers and OEMs alike, as both will need to invest significant resources in all four disruptive automotive trends.

Developments in autonomous driving, connectivity, electrification, and smart mobility are fundamentally changing the mobility sector. Mastering the underlying technologies will it make it possible for companies to extract the value of these trends. By identifying relevant technologies and investment trends in the new mobility landscape, and by cultivating an understanding of the use cases they’d like to develop and the control points they’d like to own, automotive players can then strategize about acquiring the required technology capabilities.